Cognizant's Q4 Earnings and Takeaways For Early Stage Services Businesses

Cognizant announced their 4Q22 and FY22 earnings yesterday. I thought I’d share a few observations and what early-stage services businesses may be able to take away from their results. (Disclosures: I’m not a financial advisor or analyst; this is not investment advice. I do not own any Cognizant stock and have no financial interest in the company. All images from Cognizant’s 4Q22 Investor Slides.)

☹️ Headline numbers aren't great. While Q4 and FY22 revenue was above their guide from Q3, earnings per share narrowly missed consensus expectations of $1.02. There are always revenue headwinds in Q4 because it has fewer billable days, but this most recent quarter was also worse by most measures compared to 4Q21 suggesting there is more at play than seasonality.

📉 Top-line trends have been very concerning. While revenue was growing in 2021, that growth decelerated quickly in 2022. Their 2023 Q1 guidance of -1.0% to flat revenue YoY on a constant currency basis shows that the top-line headwinds have momentum.

💰 Cognizant's book-to-bill ratio has been relatively flat for most of 2022 but did show 12% YoY growth in Q4. Cognizant also announced in January inking a 10-year renewal with CoreLogic for $1B. Assuming this deal was booked in Q1 of 2023 and not in Q4 of 2022, the Q4 growth number could bode well for Q1 being another strong quarter for bookings. However, if the deal was booked in Q4 and only announced in Q1, the pipeline picture is much fuzzier.

🥾 Leadership changes were needed. Former CEO Brian Humphries was abruptly replaced in January with Infosys veteran Ravi Kumar. Kumar was originally hired to fill a vacant position in the Americas. Other board and leadership changes have also happened, and all signs point to a feeling that the shake-up was needed to focus on growth.

🤔 Demand seems hard for leadership to gauge. From Kumar on the earnings call:

"It will take time to rebuild the pipeline and go after larger opportunities. Please know we put a lot of thought into our decision to hold off on providing full year guidance. But before making commitments I can stand behind, I really need to spend more time digging into the business and talking to associates and clients."

It's hard to tease apart how much of this is softening demand due to macro conditions vs. demand that could be there with improved sales execution.

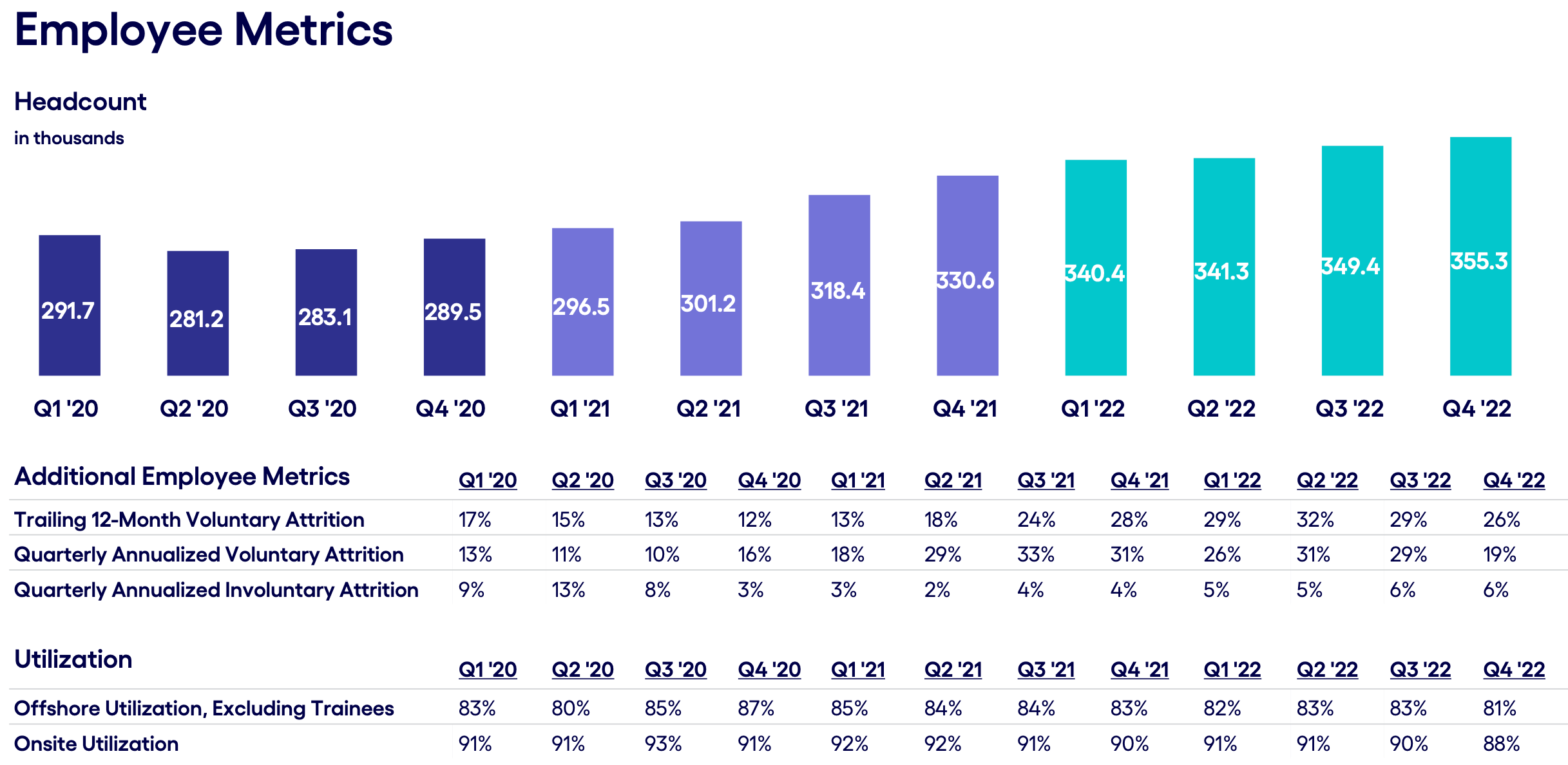

🐢 Utilization headwinds coupled with significantly slowing attrition must have hit operating margins. In Cognizant's 3Q22 earnings call, then-CEO Humphries highlighted the work leadership was doing to counteract a wave of voluntary attrition. Those efforts appear to have worked or benefited from the broader tightening of the labor market. Quarterly annualized voluntary attrition slowed from 29% in Q3 to 19% in Q4. Utilization also decreased sequentially, with offshore utilization (exclusive of trainees) going from 83% to 81%, and onshore utilization going from 90% to 88% (the lowest its been in three years). It's possible that leadership underestimated the softening of demand and overestimated the actions they needed to take to manage attrition to achieve target staffing levels.

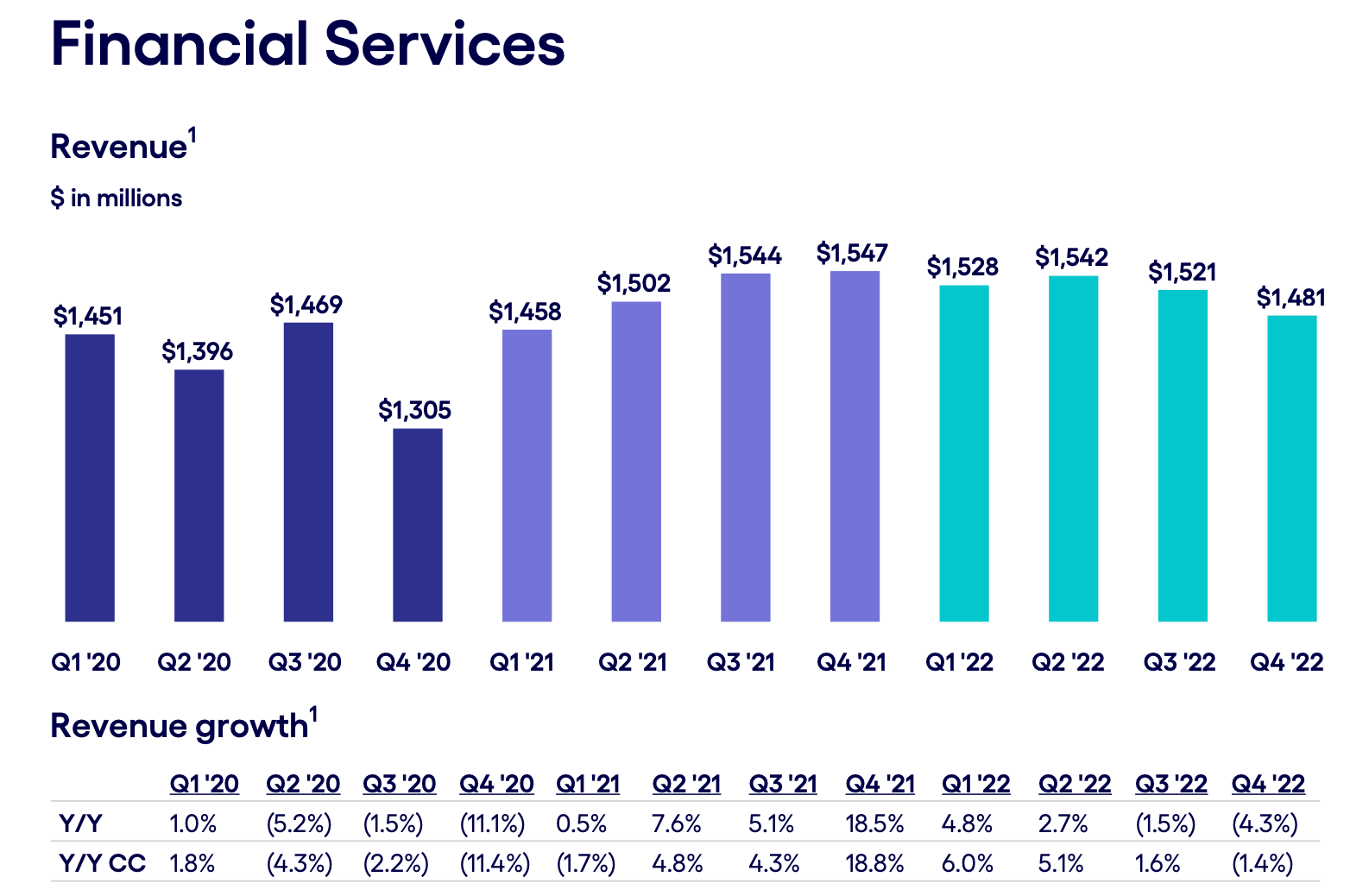

🏦 Financial services has been a particularly weak segment. Revenue shrunk 1.4% on a constant currency basis. Although some of the revenue reduction came from the sale of a subsidiary, it only explains about 40% of the decline. This segment stands out as the other three segments posted between 5.4% and 9.3% growth for the year in constant currency.

In the commentary, Cognizant also revealed that bookings declined the most in this segment as well. As a result, I suspect this weakness will persist for at least another quarter. Financial services is a very heterogenous sector in the current macroeconomic conditions: while some areas like mortgage and capital markets have been hard hit by cost-cutting, others like deposits and lending are areas of investment in the current rate environment.

The key question: is Cognizant losing deals to competitors in areas where investment is happening, or is pipeline shrinking because of concentration in areas that do poorly in high rate, potentially recessionary periods?

What should early-stage services businesses do with this information?

I think it’s helpful for early-stage businesses to see how established public companies talk about their performance and what they see happening in the market.

No early-stage company should try to emulate a public company’s predictability or governance, but there are useful cues in their analysis and the commercial trends they see.

Three things stand out to me from Cognizant’s latest earnings for early-stage services businesses:

The combination of decelerating revenue, slowing pipeline, decreasing voluntary attrition, and decreasing utilization is a powerful cautionary tale. A company the size of Cognizant has the capital to withstand suppressed operating margins for a while. And yet… even they needed to make significant changes.

Lesson: React to declining business conditions faster than you think necessary.The macro-environment may not be as bad as some people think, and digital services remain durable during economic downturns. While there was some talk of fuzzy macro factors, my read of the earnings commentary is pretty positive in that regard. Given the headwinds faced by Cognizant from factors within their control, there was reasonable constant currency revenue growth in three of their four sectors.

Lesson: If you’re doing high-value digital work, there are still many growth opportunities.If you’re competing against Cognizant in accounts where they are well-established, expect it to be brutal. There is immense focus on growth right now, and Kumar talked about wanting to do bigger deals. I would bet there will be intense competition to win every possible deal in large accounts where Cognizant already has a strong foothold. They are working on longer timelines than smaller, niche players and have an under-utilized bench that they will be eager to deploy.

Lesson: Understand the motivations of your competitors and where you may face threats inside of accounts you think are safe.

That’s it for today. This is the first time I’m sharing this kind of analysis here so I’d love your feedback. Did I miss something? Leave a comment.

Do you want to see more writing like this? Take the poll below to let me know.

Thanks for analysis Chris

Very helpful at a time we are monitoring earnings calls from customers to understand trends.