Avoiding the #1 Cause of Startup Death

It's evident that the thing that happens immediately before a business - particularly a startup - dies is that it runs out of cash. What's not apparent is why this is so often the case.

The good news is that it can usually be predicted, and founders can have more time than they realize to take action if disciplined.

Unfortunately, many founders don't take the steps needed to know when they'll run out of cash or don't take action early or aggressively enough because of lack of fiscal discipline provides a false sense of security.

Poor fiscal discipline usually arises from four underlying causes:

1. Forecasting cash in & out is less exciting than other activities to run or grow the business.

Most startup founders didn't start a business because they love jockeying spreadsheets.

Building a product, selling, talking to customers, and building a team seem much more exciting.

2. Good fiscal discipline requires accountability to variance: forecast, measure the actuals, explain the difference, and eliminate sources of inaccuracy.

There is a rhythm to good financial discipline that is only sometimes exciting to founders. Having to be honest about sources of variance and working to make them more accurate forces founders - a typically very optimistic bunch - to be realistic.

3. Good revenue metrics can conceal foundational financial performance problems... until they can't.

When things seem like they're going well, founders often don't worry about cash. If revenue is growing like a hockey stick, or the business is very capital efficient, it may feel like a waste of time. That doesn't mean you can ignore it... An analogy is measuring blood pressure: even healthy, elite athletes in their physical prime get their blood pressure checked regularly!

4. When things are going poorly, looking at the reality presented by numbers can be scary.

Sometimes founders know things are terrible. Staring at the brutal facts that predict going out of business can be terrifying.

The antidote to all these causes of business death is easy. It just requires commitment and discipline.

Step 1: Develop a month-by-month cash forecast based on anticipated payables and receivables

This is the foundation of everything else founders need to do. It must be documented. In a spreadsheet. Not on a napkin. Not in someone's head. Start with a monthly forecast for twelve months.

There will be some things that can't be precisely predicted - sales may be growing or shrinking. Hiring may go faster or slower than expected. The key is to start with a realistic set of assumptions.

If the forecast predicts having a growing cash balance, outstanding! If it doesn't, the runway needed will depend on whether the business is raising capital, bootstrapping to profitability, etc. Take note of how long the forecast predicts before running out of money. If things look dire, take action immediately.

Step 2: Review the forecast monthly

Every month, review the business' actual cash position relative to what the last forecast predicted. Record the variance, and create a new version of the cash forecast (keeping the old forecast around for future reference!).

Examine the sources of variance. Was the sales forecast too optimistic or pessimistic?

What changes are needed to make it more accurate? Adjust the assumptions made accordingly.

Were there surprise expenses? Is a larger or smaller contingency needed in the forecast? Revise the assumptions and update the forecast based on the new knowledge. Do this step every month.

Step 3: Keep an eye on the speed of the cash conversion cycle and take action when it's slowing

Forecasting receivables and expenses are only part of the equation. How quickly or slowly a sale converts to cash can starve an otherwise healthy business of the capital it needs to operate!

There are two ways to monitor this. The simple way is to review the aging of receivables by customer. Are there customers that consistently pay late? Do one or more customers have more lenient payment terms that lead to slower payment? Is a customer that had a good payment history suddenly not paying? All of these things are warning signs. Take action: following up with customers to encourage (or require) faster payment, checking in to see if there is a problem with the customer or the product leading to slow (or non-)payment, or renegotiating terms.

The slightly more quantitative way to do this is to measure Day Sales Outstanding (DSO). DSO is calculated by dividing receivables in a period by the total value of sales in the period and multiplying that by the number of days in the period. Calculating this monthly will benchmark how quickly or slowly the business is collecting receivables in aggregate and reveal trends when the speed of cash conversion changes. What makes a "good" DSO depends on the industry, but tracking DSO monthly and recording it monthly gives businesses a way to track progress when optimizing collections.

Step 4: Make the adjustments necessary when running out of runway

The first three steps will help a business accurately assess how much runway they have.

Founders need to be honest with themselves about how much runway they need. It's far more common for founders to make adjustments they need to save their business too late than too early.

If a business is getting close to having a problem, immediate action is necessary. The specific action to take - cutting expenses, securing credit, raising capital with equity, etc. - will depend on the business. Unfortunately, almost every step that will help takes longer than founders expect!

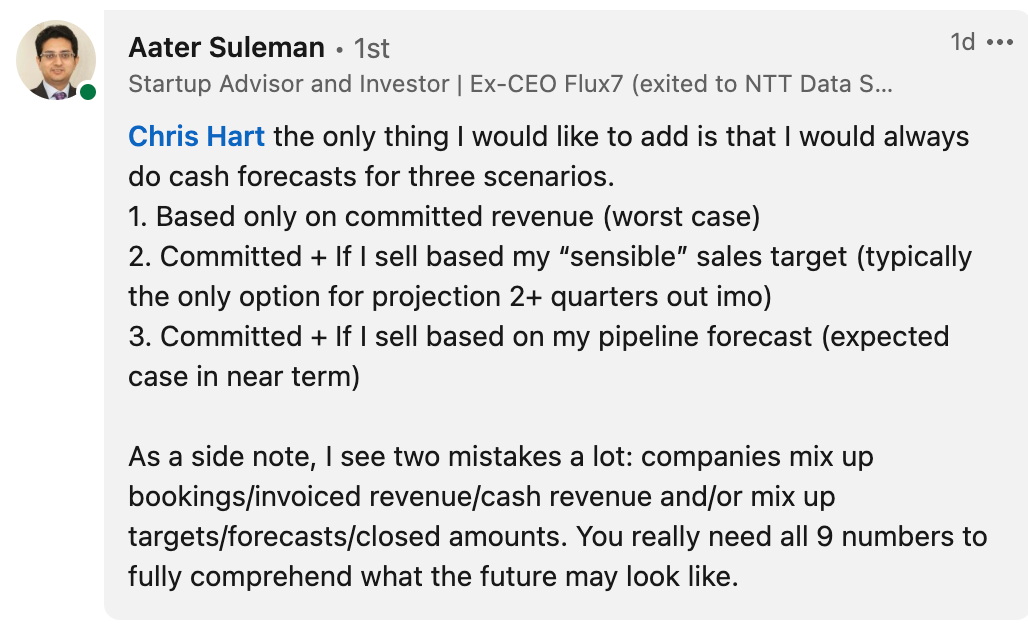

After posting a shorter version of this on LinkedIn, a few folks weighed in with some great comments that I wanted to highlight and build on. Aater Suleman commented about including multiple cash forecast scenarios:

Cash forecasting inherently relies on forecasting your sales pipeline (i.e., future revenue from sales that have not yet closed). Using historical data, like the length of the average sales cycle, the probability to close based on the deal stage, the average deal amount for a given type of sale, and so on, can make these forecasts more objective. As Aater points out, it’s not just about predicting how much is sold; predicting when revenue is collected is just as important!

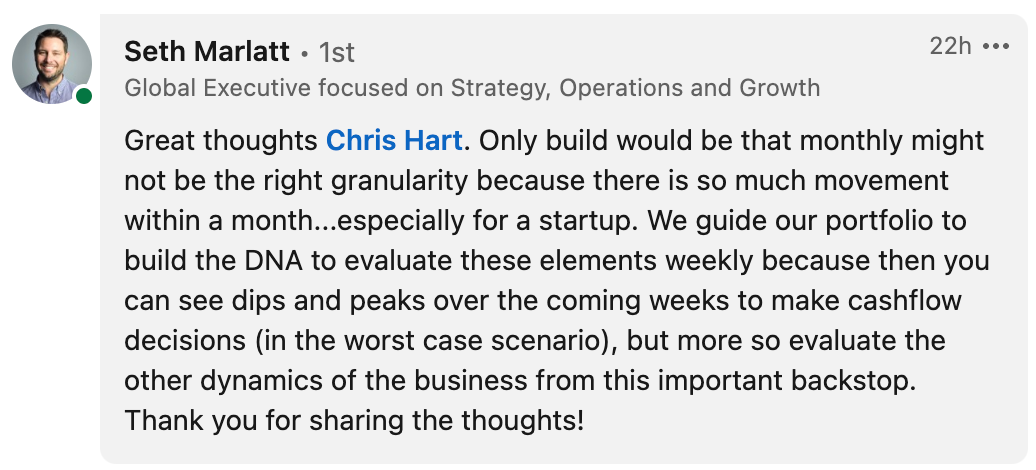

Seth Marlatt shared some insight about the benefit of looking at these metrics even more frequently:

Seth makes a great point, particularly for businesses where the tempo of sales converting, customers churning, or cash collection is fast or volatile. E.g., an early-stage SaaS business with a bottom-up sales motion probably has a lot more cash flow volatility than a managed services provider selling to enterprises. His reference to this being “DNA” is crucial: it’s important - and easier - to build these habits early.

And Jason Typrin commented about product-market fit:

This fills in the punch-line for why this is important. Financial planning is a means to an end, not an end in and of itself. Businesses that have fiscal discipline early will better manage their runway, allowing them more time to get to or refine product-market fit. And, if a business masters fiscal discipline and achieves product-market fit, you will have (some) tools that enable you to scale more efficiently or generate better profitability.